Workflow Automation in Banking Explained

January 16, 2026 By Yodaplus

Banks run on processes. Every account opening, loan approval, payment, compliance check, and report follows a defined workflow. For decades, these workflows relied on manual handoffs, emails, spreadsheets, and fragmented systems. As transaction volumes increased and regulations tightened, these manual processes became harder to manage. Workflow automation in banking addresses this problem by replacing manual coordination with structured, system-driven flows. It ensures tasks move forward consistently, decisions follow rules, and outcomes remain traceable.

What workflow automation means in a banking context

Workflow automation in banking is not about replacing people with software. It is about defining how work moves across teams, systems, and approvals. A workflow describes steps, decision points, dependencies, and outcomes. Automation executes this workflow automatically. For example, when a customer submits a loan application, the workflow routes it through credit checks, document verification, risk assessment, approvals, and disbursement without relying on emails or follow-ups. Each step triggers the next based on rules and data.

How banking workflows differ from other industries

Banking workflows differ because they operate under strict regulatory and risk constraints. Every action must be auditable. Every decision must follow policy. Exceptions must be justified and recorded. Unlike retail or manufacturing, banks cannot bypass steps for speed alone. Workflow automation in banking must balance efficiency with control. This is why banking automation focuses heavily on approvals, validations, and compliance checkpoints rather than simple task acceleration.

Core areas where workflow automation is used in banking

Workflow automation spans almost every banking function. In retail banking, it supports account opening, KYC verification, customer onboarding, and service requests. In corporate banking, it handles credit approvals, limit management, and trade finance workflows. In payments, it manages transaction validation, exception handling, and reconciliation. In compliance, it coordinates audits, reporting, and regulatory submissions. These workflows often cross departments, making automation essential for consistency.

Account opening and customer onboarding workflows

Customer onboarding is one of the most visible banking workflows. It includes identity verification, document collection, risk checks, and account activation. Manual onboarding leads to delays and errors. Workflow automation standardizes this process. When a customer submits documents, the system validates them, routes them for review if needed, and tracks progress. Automation ensures no step is skipped and no approval happens without required checks. This improves customer experience while maintaining compliance.

Credit and lending workflows

Lending workflows involve multiple evaluations. Credit assessment, collateral checks, pricing approvals, and risk reviews must happen in sequence. Workflow automation ensures these evaluations occur in the correct order. It enforces approval hierarchies and applies credit rules consistently. When conditions change, such as updated financial data or policy changes, workflows adapt without manual intervention. This structure reduces turnaround time while preserving credit discipline.

Payment and transaction workflows

Banking transactions generate exceptions. Failed payments, suspicious transfers, and reconciliation mismatches require structured handling. Workflow automation routes these exceptions to the right teams based on severity and type. Instead of relying on inboxes, automated workflows ensure timely resolution and proper documentation. This reduces operational risk and improves settlement accuracy.

Compliance and regulatory workflows

Compliance is central to banking operations. Regulatory reporting, audits, and internal controls follow defined schedules and procedures. Workflow automation ensures tasks happen on time and evidence gets recorded. When regulators request information, automated workflows provide traceable records. This reduces compliance burden and improves readiness during audits.

Role of data in workflow automation

Data drives automated workflows. Banking systems generate large volumes of transactional and customer data. Workflow automation uses this data to trigger actions and decisions. For example, a transaction above a threshold may trigger additional checks. A missed repayment may initiate a follow-up workflow. Data-driven workflows react in real time, reducing delays and manual monitoring.

Integration with core banking systems

Workflow automation does not replace core banking systems. It sits above them. Core systems store accounts, transactions, and balances. Workflow engines orchestrate how tasks interact with these systems. Integration ensures workflows can read data, trigger actions, and update records without duplication. This layered approach allows banks to modernize processes without replacing legacy systems immediately.

Exception handling as a core design principle

No banking workflow runs perfectly. Exceptions are normal. Failed validations, missing documents, or policy overrides occur daily. Effective workflow automation designs for exceptions instead of ignoring them. It routes exceptions to the right role, applies escalation rules, and records outcomes. This prevents manual chaos and ensures exceptions do not stall the entire process.

Security and access control in automated workflows

Banking workflows must enforce access controls. Not every employee can approve every action. Workflow automation embeds role-based permissions directly into processes. Only authorized users can perform specific actions. Every action leaves an audit trail. This improves security and reduces insider risk.

Measuring success of workflow automation

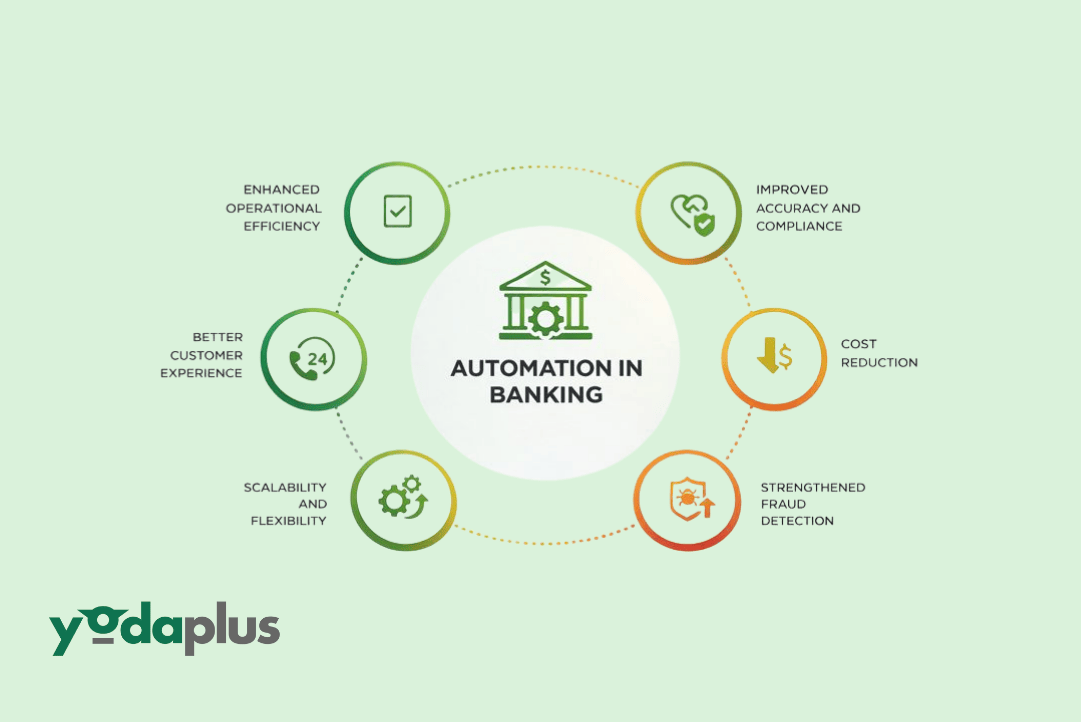

Banks measure workflow automation success through operational metrics. These include turnaround time, error rates, exception volumes, and compliance outcomes. Automation reduces processing time and manual errors. It also improves visibility. Managers can see bottlenecks and optimize workflows continuously. This feedback loop helps banks refine processes over time.

Challenges in implementing workflow automation

Workflow automation requires clarity. Poorly defined processes lead to poor automation outcomes. Banks often struggle with fragmented ownership, outdated policies, and inconsistent data. Successful implementation starts with process mapping and stakeholder alignment. Automation then enforces agreed rules rather than creating new ones. Change management is equally important to ensure adoption.

How workflow automation supports digital banking goals

Digital banking depends on fast, reliable processes. Customers expect instant responses and transparent status updates. Workflow automation enables this by connecting front-end channels with back-end systems. Automated workflows power self-service, reduce response times, and improve consistency. This alignment supports long-term digital transformation goals.

FAQs

Is workflow automation the same as robotic process automation?

No. Workflow automation orchestrates processes and decisions. Robotic automation handles repetitive tasks.

Does workflow automation reduce human involvement?

It reduces manual coordination, not human judgment. People still review and approve critical steps.

Can workflow automation work with legacy banking systems?

Yes. It integrates with existing systems through APIs or service layers.

Is workflow automation only for large banks?

No. Mid-sized and regional banks often benefit the most due to limited operational staff.

Final thoughts

Workflow automation in banking creates structure where complexity already exists. With Yodaplus Automation Services, banks replace manual coordination with predictable, auditable flows. By automating how work moves across teams and systems, institutions improve efficiency without compromising control. Workflow automation is not a shortcut. It is a foundation for scalable, compliant, and resilient banking operations.